Last Updated on January 24, 2023 by Chicago Policy Review Staff

It is no secret that the rich hate paying taxes. A recent ProPublica investigation of tax returns revealed that the 25 richest Americans paid a true tax rate of 3.4% on the wealth they accumulated from 2014 to 2018 through entirely legal means. At the same time, there are troves of wealthy Americans who find complex ways to underreport their income illegally. The Department of Treasury estimates that in 2019, the amount of tax that should have been collected, but was not, amounted to $600 billion. Our tax code benefits the rich because the income they earn disproportionately comes from non-labor income streams that are both taxed at lower rates and more difficult for the IRS to verify. As a result, the top 1% is responsible for 36% of all unpaid individual income taxes annually.

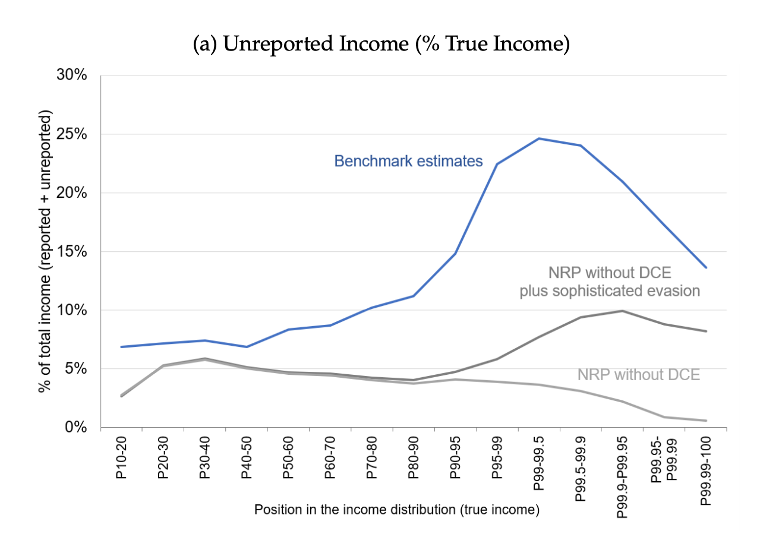

A recent paper published by John Guyton, Patrick Langetieg, Daniel Reck, Max Risch, and Gabriel Zucman illuminates the extent to which ultra-wealthy Americans – those in the top 0.01% – evade taxes. The IRS produces official estimates of tax evasion by using data from their random audit program, the National Research Program (NRP), to determine who is evading taxes and how much they owe. The authors point out that these random audits do not detect all forms of tax evasion at the same rate. Identifying more complex forms of evasion typically requires additional information. The imperfect random audits produce a set of data that shows tax evasion increases alongside income, declines for the top 1%, and drops off further for the top 0.01%. The authors set out to determine whether the top 0.01% evade fewer taxes or if they’re just better at hiding it.

Guyton et. al. identify two forms of tax noncompliance typically missed by random audits due to resource limitations on auditing complex evasion: offshore and pass-through tax evasion. Unsurprisingly, the wealthiest Americans utilize these two forms of tax evasion more than taxpayers in the bottom 90%. The authors attempt to overcome the informational limitations of the NRP audits on offshore evasion by including information from U.S. taxpayers who voluntarily disclosed offshore accounts as part of a specific enforcement initiative in 2008-2009. In the case of pass-through misreporting, the NRP audits identify misreporting in only 3.8% of cases. Meanwhile, NRP audits more comprehensively examine sole proprietorship income and find a 37% underreporting rate. The authors make several assumptions about how pass-through misreporting rates should really be in between misreporting rates for sole proprietors and corporations, and as a result, they settle on a rate of 20%.

Guyton et. al present their own model, which supports the assertion that random audits likely underestimate the amount of taxes evaded by the wealthy. Overall, they find that the top 1% underreport 21% of their income, 6% of which can be attributed to sophisticated methods of evasion that random audits miss. This is three times greater than what the median taxpayer underreports. They also find tax evasion rates are twice as high in the top 0.01% wealth-owners as the previous data suggested. Their analysis reveals that the 14,000 families making more than 11.9 million annually (top 0.01%) are not actually more honest – they are simply better at evading taxes.

The reasons the rich have an easier time avoiding taxes are plentiful. In general, tax compliance rates are highly correlated with the extent to which third party information reporting is available. Low- and middle-income taxpayers typically have income streams, like wages and Social Security benefits, along with strong third-party information reporting. In the case of wages, the IRS can easily determine if a taxpayer misreported their income by cross referencing the corresponding W-2 form shared by their employer. As a result, wage-earners misreport 1% of their income. High-income taxpayers, on the other hand, rely on income streams with less third-party information reporting, like proprietorship and rental income. For these kinds of highly opaque income streams, the misreporting rate is approximately 55%.

A decade of depleted budgets for enforcement, aging technology, and staff that is not equipped to detect sophisticated tax evasion strategies have contributed to the recent decrease in audit rates on the wealthy. Guyton et. al.’s estimates of tax noncompliance at the top of the income distribution suggest that investing in tax enforcement efforts could produce even larger returns than previously anticipated. By collecting all the unpaid taxes owed by the top 1%, the authors suggest that the government would raise an additional $175 billion every year – without increasing taxes.

Closing the tax gap would help address rising wealth inequality in the U.S. by reining in the top 1%. It is also a way to finance meaningful social programs that benefit lower- and middle-classes. In fact, President Biden’s American Families Plan includes tax compliance provisions to raise revenue for its investments in childcare and free pre-K. The Treasury’s proposal claims that an $80 billion investment would yield $700 billion in additional revenue over the next decade.

For many, raising taxes on the rich is the first solution that comes to mind when deciding how to make the tax code more just, though additional measures are required to fix the larger problem of tax evasion. We need to make critical investments in technology and the IRS workforce to detect more sophisticated forms of tax evasion and collect what is already owed. There’s a clear return on investment: every $1 we invest on tax enforcement yields at least $4 in recouped taxes. Closing the tax gap is only the first step towards creating a more equitable tax system that rewards the majority of honest taxpayers and deters the wealthiest taxpayers from shirking their tax bills.

Eisinger, Jesse, Jeff Ernsthausen, and Paul Kiel. 2021. “The Secret IRS Files: Trove of Never-Before-Seen Records Reveal How the Wealthiest Avoid Income Tax.” ProPublica, June 8, 2021. https://www.propublica.org/article/the-secret-irs-files-trove-of-never-before-seen-records-reveal-how-the-wealthiest-avoid-income-tax

Guyton, John, Patrick Langetieg, Daniel Reck, Max Risch, and Gabriel Zucman. 2021. “Tax Evasion at the Top of the Income Distribution: Theory and Evidence.” NBER Working Paper No. 28542. https://www.nber.org/papers/w28542, accessed June 2021.

The U.S. Department of the Treasury. 2021. “The American Families Plan Tax Compliance Agenda.” https://home.treasury.gov/system/files/136/The-American-Families-Plan-Tax-Compliance-Agenda.pdf